If a tornado just tore through your part of Tuscaloosa, you’re probably dealing with a damaged roof, an insurance claim that’s just getting started, maybe a temporary place to stay, and a house you’re not sure is even worth fixing. In the middle of all that, one question keeps coming up: do you repair it, or how to sell a tornado damaged house in Tuscaloosa right now?

You have more options than it might feel like at the moment. Broadly, there are three paths: repair the home and list it with an agent, list it as-is on the open market, or sell as-is to a cash buyer or investor. Which one makes sense depends on your insurance situation, how much time and cash you have, and honestly, how much more you want to deal with right now.

This guide walks through each path in practical terms, what FEMA and SBA assistance can and can’t do, and what to watch for along the way. This is educational information, not legal, tax, or insurance advice.

In the first hours and days after a storm, the priorities are simple: get to safety, document everything, and keep every receipt. Once you have a clearer read on your insurance status and the actual condition of the house, you can start mapping out which path fits.

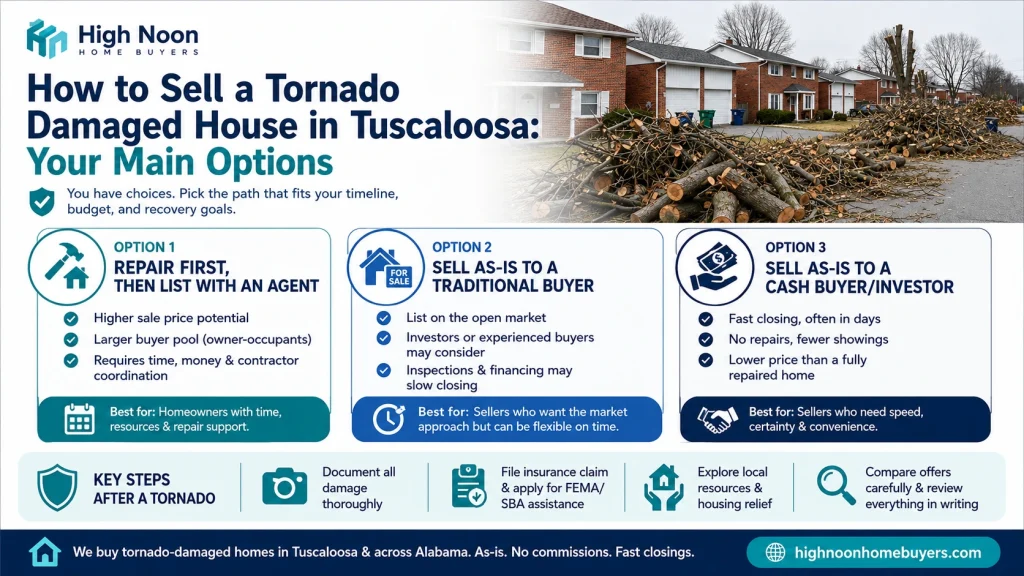

Repair first, then list with an agent: This makes the most sense when insurance is covering most of the repair cost and you have the time to manage contractors and inspections. A fully repaired home opens you up to the widest buyer pool, including owner-occupants using conventional, FHA, or VA loans, and it typically sells for more. The tradeoff is upfront cash, contractor coordination, and weeks or months before you’re even ready to list.

List as-is on the open market: Some traditional buyers, often investors or experienced purchasers, will look at a damaged property without requiring full repairs first. This keeps the process more familiar, an agent, a listing, negotiations, but it can still involve inspections, repair-credit negotiations, and financing contingencies that slow things down.

Sell as-is to a cash buyer or investor: This route makes the most sense when repairs are too expensive to front, the house isn’t really safe or presentable to show, or you just want to move on without managing another project. Because there’s no mortgage contingency, closings tend to move faster and depend less on a lender’s timeline. You’ll typically net less than a fully repaired sale, but you also skip the showings, the contractor calls, and the waiting.

A note on red flags, after any disaster, there are people looking to take advantage of homeowners under pressure. Be cautious of anyone pushing you to sign over your deed immediately, anyone who won’t put terms in writing, requests for big fees upfront, or buyers who won’t show proof of funds or their legal identity. Use a licensed closing attorney or title company, and have any contract reviewed before you sign, no matter how easy the buyer makes it sound.

For a lot of Tuscaloosa homeowners, a cash buyer ends up being the most practical fit specifically because of what tornado damage looks like up close: debris still in the yard, a roof that’s tarped but not fixed, an insurance claim that’s still open, maybe a temporary place to stay while you figure things out. A cash sale means you don’t have to finish repairs, clean up debris, or host multiple showings while you’re also juggling all of that.

It also gives you more flexibility if you need to leave some personal property behind, or need a little extra time before you move. The tradeoff is that the sale price will usually be lower than what a fully repaired, listed home would bring, and the cash-buyer pool includes some wholesalers and contract-assigners who aren’t always upfront about who’s actually closing on your house, so it’s worth vetting carefully. Not every cash buyer operates the same way, and a few honest questions upfront will tell you a lot.

Before you start talking to buyers, gather what you’ll need anyway: dated photos and video of the damage, your insurance claim status and any adjuster or contractor estimates, FEMA or SBA paperwork if you’ve applied, and your property tax bill or deed.

When you do talk to a buyer, ask directly: Can you show proof of funds? Who actually appears on the title at closing? Are there any fees or commissions? What’s your realistic closing timeline, and what could push it back? Will you assign or resell this contract to someone else? A local Tuscaloosa investor who’s worked through Alabama tornado recovery before will usually navigate things like an open insurance claim or unfinished repairs more smoothly than someone from out of state who’s never dealt with it.

You don’t need an insurance textbook here, just the basics that actually affect your sale. File your claim, document the damage thoroughly, and get a clear picture of what’s already been paid out versus what’s still pending. Buyers, cash or traditional, will want to know exactly that before making an offer: what repairs are done, what’s left, and whether insurance money is still in process.

In Alabama, wind damage from a tornado is usually covered under a standard homeowners policy, but the specifics depend on your actual policy language, so don’t assume anything without checking. If you do end up talking to buyers with an open claim, something as simple as “we have an open claim and expect certain repairs before closing” or “we’ve received our payout and are selling as-is” tells them exactly where things stand.

A couple of programs are worth knowing about if a disaster declaration applies to your area. FEMA’s Individual and Households Program can help with repairs, temporary housing, or essential personal property, but it doesn’t duplicate what insurance already covers, so you’ll generally need to file your insurance claim first.

The SBA also offers disaster loans that can help bridge the gap between what insurance pays and what repairs actually cost. And if you run into delays or disputes with your insurer, the Alabama Department of Insurance has a consumer-help line and complaint process. For anything specific to your policy or claim, your insurer or a licensed Alabama attorney is the right call, not a guess.

Start with the Tuscaloosa County Emergency Management Agency, they’re the local hub for damage assessments and recovery guidance specific to your area. If you need help with housing or other local support, Alabama 211 connects you to disaster-recovery centers and services. From there, if a federal disaster declaration applies, FEMA’s IHP and SBA disaster loans become worth looking into, and HUD has housing counseling and mortgage-relief options if you’re carrying a loan on the damaged property. If your insurer is dragging its feet, ALDOI’s consumer resources can help.

Whichever resources you end up using, you’ll want the same documents on hand: dated photos and video, contractor estimates if you have them, your insurance policy number and claim info, any FEMA or SBA paperwork, your property tax bill or deed, and any damage assessment paperwork from TCEMA. And a quick word of caution: after a disaster, scams show up fast. Stick to official .gov sites or verified nonprofits, call published phone numbers rather than ones from a text or flyer you didn’t ask for, and never pay a large fee upfront just to access assistance.

It really comes down to whether you have the time, the cash, and the insurance support to get through repairs, or whether that feels like more than you want to take on right now.

Repair first if insurance is covering most of the cost, you have weeks or months to manage contractors and inspections, and a higher sale price matters more to you than speed. Sell as-is if the repairs are overwhelming, the home isn’t safe to show, your claim is still unresolved, or you just want this chapter closed without managing another project on top of everything else life is already throwing at you.

One thing worth knowing either way: selling as-is means the buyer accepts the property’s current condition at closing, with full disclosure. It doesn’t mean you can hide known problems, you still have to be upfront about what’s wrong.

You don’t need to become a tax expert to sell your house, but a few things are worth flagging before you close. Insurance proceeds, repair costs, and your final sale price can all interact in ways that affect what you owe, and there are IRS rules around involuntary conversions that may let you defer some of that gain if you reinvest in a similar property, plus separate rules for primary residences that can exclude a chunk of any gain entirely. The short version: talk to a tax professional before closing, they can tell you exactly how your situation shakes out.

If you’re carrying a mortgage, HUD and your servicer may offer forbearance or a pause on foreclosure proceedings in a declared disaster, worth asking about if that’s relevant to you. And as a seller in Alabama, you do have disclosure obligations around known material defects, so a real estate attorney or licensed broker can walk you through exactly what needs to be disclosed for your specific sale.

Safety comes first, always. Follow guidance from TCEMA and local officials, stay away from downed power lines or anything that looks structurally unsafe, and get yourself somewhere stable before worrying about anything else.

Once you’re safe, document everything before you touch anything. Take dated photos and video from multiple angles, and don’t start throwing things away until you’ve captured it all. Keep every receipt, emergency repairs, cleanup, temporary housing, and start one folder for your storm paperwork: policy info, claim numbers, adjuster reports, FEMA or SBA forms. Insurance, FEMA, buyers, and contractors will all ask for this stuff eventually, and having it in one place will save you real headaches later.

From there, file your insurance claim promptly, register with FEMA if applicable, and apply for an SBA loan if it makes sense for your situation. Delays in filing can cost you time and options down the road. Look into HUD housing counseling or mortgage relief if you’re trying to figure out whether to rebuild, repair, or sell, and lean on Alabama 211 for local support along the way.

Once you’ve got your documentation together and a sense of where insurance stands, start talking to agents or cash buyers, and talk to more than one before you commit to anyone. When offers come in, compare them carefully: price, who covers closing costs, who handles remaining debris or repairs, the actual timeline, and whether the contract can be assigned to someone else. Have an attorney look it over before you sign anything. And when you’re ready to plan your move, TCEMA, Alabama 211, FEMA, and HUD can all help you coordinate that transition before you finalize a closing date.

Can I sell my tornado-damaged house in Tuscaloosa without fixing it first?

Yes, you can sell without fixing it first, but your buyer pool, price, and timeline will depend a lot on how much damage is still visible and what’s happening with your insurance claim. Full disclosure and staying in close contact with your insurer matter no matter which path you choose.

Will my insurance payout affect my sale price or how fast I can close?

It can affect both. Buyers want to know what damage remains, what’s already been repaired, and whether any insurance money is still pending. Stay in close contact with your insurer and, if it applies, FEMA or SBA, and talk to a tax professional about how the proceeds and sale price interact before you close.

What should I ask a cash buyer in Tuscaloosa?

Ask for proof of funds, their actual closing timeline and what could delay it, whether they charge any fees or commissions, whether they plan to assign or resell the contract, and what condition they expect the house to be in at closing. Get everything in writing before you sign.

What local resources are worth knowing about after a tornado?

TCEMA handles local damage assessments and recovery guidance. Alabama 211 connects you to housing and support services. FEMA’s IHP, SBA disaster loans, HUD housing counseling, and ALDOI’s consumer resources round out the bigger-picture options if a disaster declaration applies to your area.

Recovering from tornado damage is never easy, but you do have real choices here, whether that’s repairing and listing, selling as-is on the open market, or working with a cash buyer. The right call depends on your timeline, your finances, and how much coordination you genuinely have the bandwidth for right now.

If the repairs, the insurance process, or the cleanup feel like more than you want to manage, High Noon can walk through the as-is option with you and give you a no-pressure cash offer. We buy tornado-damaged homes in Tuscaloosa and across Alabama, no repairs required, no commissions, and on a timeline that fits your recovery. Reach out to highnoonhomebuyers whenever you’re ready.